Classes of Nickel and Where to Find Them

Setting eyes on Indonesia.

Lithium has gotten a lot of attention lately due to its rapid increase in price since January of 2018 to nearly $70,000 per ton (below). The surge in electric vehicle demand coupled with geopolitical tensions has various parties speculating where the price will go from here.

The percentage increase in price for various battery raw materials has been most pronounced for lithium, but we should not take our eyes off of the other metals. A 50-100% increase in price for other transition elements and active materials is nothing to ignore.

In my latest independent contribution to Intercalation, I dove into nickel which was spurred by reading a recent report from the International Energy Agency. Nickel in and of itself is a complex mineral, because it is found in various forms in mines throughout the world. The challenge is that it may be at the forefront for some time, because a large part of the class I nickel market is supplied from Russia.

Russia is the largest independent contributor and holds about 20% of the class I market share. It also maintains a strong position in the refining of lithium as shown in the pie graph below.

The attacks that occurred earlier on in the year caused the dramatic price spike of nickel. Over the past few months thankfully the price of Ni has subsided, but the threat of supply constraints do not disappear.

Class I and II Nickel

Class I nickel is very important for the lithium ion battery industry because of its purity. Class II contains various contaminants that make it unsuitable for use in lithium ion batteries. Class II has long been supplied to the stainless steel industry and provides benefits due to its high iron content.

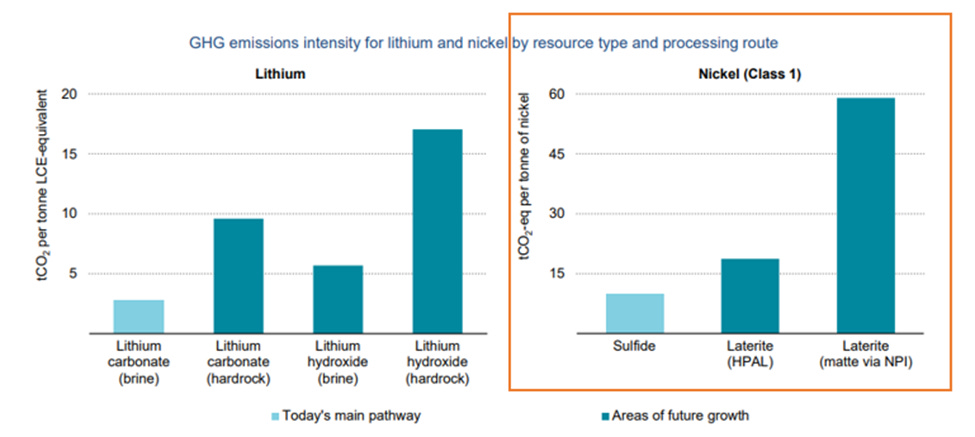

While more class I nickel can be produced by further purifying class II nickel sources, these are much more energy intensive. HPAL (high performance acid leaching) and extraction from nickel pig iron use heat and/or hydrometallurgical washing processes to clean the dirtier laterite layers (where class II comes from) of the Earth. At the moment, significantly higher amounts of greenhouse emissions are created from these advanced purification processes as shown in the image below. It signals the need to further improve the efficiency of lower grade nickel ore refining. Fitch Solutions identifies various HPAL projects going on throughout the world.

A Challenge to Produce More Class I

The country of Indonesia is the leader in class II nickel mining and also holds the most reserves at roughly 20 million tons. If various extraction processes can be implemented and executed in a reasonable amount of time, I believe that they could help stabilize the class I nickel market.

It is well known that the global supply chain has been strained for some time now and costs are rising. A recent article shows how essentially every mineral in the electric vehicle supply chain has been impacted.

It is not just nickel. It is mining in general that needs a resurgence. As much as we can say it mining takes time and multiple parties and interests need to be taken into consideration.

Want to dive deeper? Check out the piece on Intercalation, a leading blog in the batteries and renewable space.

References:

1) Global Supply Chains of EV Batteries. International Energy Agency. July 2022

2) The Role of Critical Minerals in Clean Energy Transitions. International Energy Agency. May 2021

3) Battery Grade Nickel: Assessing Global Supply Bottlenecks and Opportunities. Fitch Solutions. Dec 2021

4) “What is Driving Lithium Prices in 2022 and Beyond.” Benchmark Mineral Intelligence. August 2022.

5) Raw material costs...doubled during the pandemic. CNBC. June 2022